SGH LaSalle Concentrated Global Property Fund – Quarterly Update

March quarter 2024, Matt Sgrizzi

Fund performance and key drivers*

The back and forth in markets continued, with concerns about stubborn inflation earlier in the quarter weighing on markets. Then the Central bank dovishness later in the quarter offsetting that weakness. Global REITs echo that dynamic, and we’re perfectly flat on the board.

Our fund, SGH LaSalle Concentrated Global Property, also performed very similarly and was flat to the index for the quarter. That brings our trailing one-year return to 8.5 percent or 70 basis points better than the GREIT Index. Since we began the strategy 4+ years ago, we’ve outperformed the GREIT Index by 700 basis points annually.

How is the portfolio positioned?

The portfolio is positioned to only invest in the best real estate opportunities we see globally. Lately, that’s been a broad mix of real estate investment companies with some of our largest overweight positions and nontraditional property types like cell towers, billboards, triple net lease, and single-family homes.

These sectors give investors the key benefits of real estate ownership, with differentiated and structurally attractive growth profiles and attractive risk-adjusted returns.

We also have meaningful exposure to REITs and traditional property types like apartments, retail, logistics sheds, and even the unloved office sector. Many reasons these sectors are poised to benefit from what will likely be a very favourable supply setup as development has been curtailed in these sectors as demand is expected to remain stable in these sectors, they will likely enjoy favourable fundamentals.

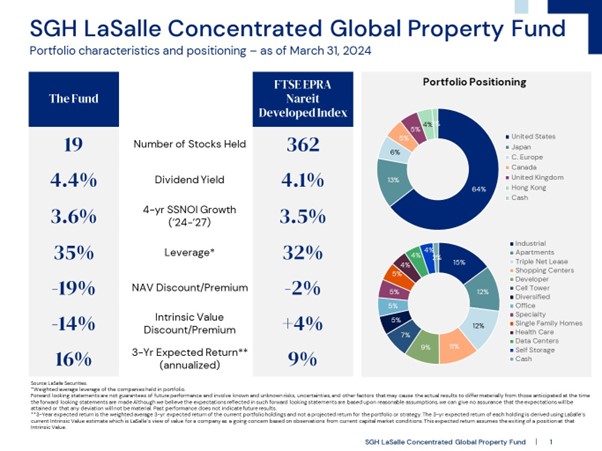

To show some high-level information on our portfolio positioning, today:

- we hold just 19 stocks with

- an attractive dividend yield of 4.4%;

- very strong forecasted unlevered cash flow of about 3.6% per year over the next four years;

- modest leverage of 35% loan-to-value;

- significant discount to private market values; and a similar

- healthy discount to our primary valuation metric, intrinsic value (derived from capital market-based discounted capital model that values these companies as going concerns).

We underwrite to an attractive 16% annualised return for this portfolio on a third-year hold as well, reflecting the high-end places and growth for the company’s portfolio.

Note especially that on our key valuation metrics of intrinsic value and expected return, the portfolio is far more attractive than the universal GREITs represented by the FTSE Real Estate Index. Also note that 64% of the portfolio is invested in the US with Japan the next largest exposure and they have very good diversification across truly unique property types.

Has the positioning changed during the quarter?

We had a couple of meaningful changes in the portfolio during the quarter, we changed preference for our holding in the self-storage sector after benefiting from a non-consensus position in the fourth quarter last year.

We also added to a new position in London office. UK REITs are off to a weak start in the year, with interest rates bouncing back up and we see this as an opportunity to get back into the UK office REITs, which are heavily discounted.

Although the headwinds facing the office sector are well known, good quality space is leasing up very well now, and we even see market rents starting to tick up. Businesses are using their office space differently today after COVID, but they all want good space that is well connected, needs high environmental specifications, and are generally places that people just want to be. And those principles underline the UK holding that we added in the quarter.

Why invest in GREITs now?

Number one, GREITs have repriced since the market peaked at the end of 2021. Listed real estate is priced much more fairly in the public market than in the private market, where appraisals continue to lag reality.

We would say unequivocally that any investor looking to allocate capital to alternatives should do so in public markets before even thinking about allocating to private markets.

Second, the outlook for real estate fundamentals is very solid, underpinned by several dynamic real estate sectors that are enjoying strong pricing power and limited or declining levels of competitive supply. REITs are also in very strong capital position and are poised to grow their market share compared to private investors who are more dependent on debt finance.

Finally, the track record for this phone has been very strong. And we’ve proven our ability to outperform in up and down markets where we’re a challenging time period. With an unrelenting focus of only investing in the best opportunities we see in the global real estate markets, we expect to continue to prove that we can help investors navigate the global markets while retaining the many benefits including liquid real estate in their portfolios.

Click here to find out more about the fund.

*The text has been edited for clarity.

The document contains general information only. Reference to either individual securities or other investments should not be considered as investment advice. We strongly encourage you to obtain professional advice before making an investment in securities that have been mentioned. Documents you should consider prior to making an investment could include the relevant Product Disclosure Statement and the accompanying Target Market Determination. If you would like further information on financial products that SG Hiscock & Company Ltd (AFSL 240679) is the investment manager for, contact the Client Services team on 1300 133 451, visit the website www.sghiscock.com.au or contact your financial adviser. Any investment is subject to risk, including possible loss of income or capital invested.